The 1% rule is dead (here's what to use instead)

The 1% rule worked in 2015. In 2026, it filters out good deals and gives false confidence on bad ones. Learn the metrics that actually matter.

If you have spent any time learning about real estate investing, you have heard the 1% rule. Monthly rent should equal at least 1% of the purchase price. A $200,000 property should rent for $2,000 per month.

It is simple. It is easy to calculate. And in 2026, it will cause you to pass on profitable deals and feel confident about bad ones.

The 1% rule made sense when properties were cheaper relative to rents. Today, in most markets, it simply does not exist. Waiting for a property that hits 1% means waiting forever in many areas.

Here is what to use instead.

Why the 1% rule stopped working

The 1% rule emerged when home prices were lower and rents had not caught up to price appreciation. In many Midwest and Southern markets through the 2010s, you could reliably find properties that hit or exceeded 1%.

Then prices exploded.

Between 2020 and 2024, median home prices increased over 40% nationally. Rents increased too, but not at the same pace. The math stopped working.

Where the 1% rule still works: Select markets in the Midwest and Southeast with lower price points. Think smaller cities in Ohio, Indiana, Missouri, and parts of the South.

Where it does not work: Most coastal cities, major metros, and anywhere prices have run up significantly. San Francisco, New York, Los Angeles, Denver, Austin, and dozens of other markets will never hit 1%.

If you limit yourself to the 1% rule, you eliminate most of the country from consideration.

The problem with simple rules

The 1% rule tries to answer a complex question with a simple ratio: "Will this property cash flow?"

But cash flow depends on many factors the 1% rule ignores:

- Interest rates: A property at 0.9% might cash flow great at 5% interest but lose money at 7%

- Property taxes: A $2,000/month property in Texas pays very different taxes than one in Florida

- Insurance costs: Coastal properties or older homes have higher insurance

- HOA fees: Condos with $400/month HOA eat into cash flow

- Vacancy rates: A 10% vacancy assumption changes everything

- Maintenance: Older properties cost more to maintain

Two properties with identical rent-to-price ratios can have completely different cash flows. The 1% rule hides this reality.

What to use instead

The solution is not a different simple rule. It is using multiple metrics that each tell you something specific about the deal.

Cash-on-Cash Return (CoC ROI)

What it measures: Your annual cash return divided by the total cash you invested.

Why it matters: This is your actual return on the money you put in. A property might "fail" the 1% rule but deliver 8% cash-on-cash return. Another might "pass" but only return 3%.

Typical targets in 2026:

- 6-10%: Common conservative range

- 8-12%: Aspirational, harder to achieve at current rates

- Below 6%: May not be worth the effort and risk

Example: You invest $60,000 total (down payment + closing costs) and receive $4,800/year in cash flow. Your cash-on-cash return is 8%. The 1% rule never tells you this number.

Cap Rate (Capitalization Rate)

What it measures: Net operating income divided by purchase price. This shows the property's return as if you paid all cash.

Why it matters: Cap rate removes financing from the equation. It lets you compare the property's intrinsic income potential regardless of how you structure the loan.

Typical ranges in 2026:

- 4-6%: Common in high-demand, appreciating markets

- 6-8%: Balanced markets with moderate appreciation

- 8%+: Higher income relative to price, often in less appreciating areas

The tradeoff: Low cap rate markets often have higher appreciation potential. High cap rate markets often have lower appreciation but better cash flow. Neither is universally better.

Debt Service Coverage Ratio (DCR)

What it measures: Net operating income divided by annual debt payments. Shows whether rental income covers your mortgage.

Why it matters: DCR tells you how much cushion you have. A property can pass the 1% rule but have a DCR of 1.05, meaning one unexpected expense wipes out your margin.

What lenders require:

- 1.20-1.25: Most lenders' minimum requirement

- 1.0-1.2: Tight margin, less room for error

- Below 1.0: You are losing money every month

Break-Even Ratio

What it measures: What percentage of potential rent you need to collect to cover all expenses and debt.

Why it matters: This shows your vacancy tolerance. A break-even ratio of 70% means you can handle 30% vacancy and still cover costs. A ratio of 90% means any vacancy hurts immediately.

What to look for:

- 80% or below: Comfortable cushion

- 80-90%: Moderate margin, workable but tight

- Above 90%: Very little room for vacancy or surprises

Putting it together: two properties compared

Let's compare two properties side by side. One passes the 1% rule. One fails it.

Assumptions for both properties:

- Vacancy: 5%

- Property management: 10% of rent

- Closing costs: 3% of purchase price

- 30-year fixed mortgage

Property A: Passes the 1% rule

- Purchase price: $180,000

- Monthly rent: $1,800 (exactly 1%)

- Property taxes: $4,200/year (2.3% rate)

- Insurance: $1,800/year (older property, coastal area)

- Maintenance reserve: $150/month (older property needs more upkeep)

- 25% down at 7% interest

Monthly breakdown:

- P&I: $898

- Taxes: $350

- Insurance: $150

- Maintenance: $150

- Property management: $180

- Total expenses: $1,728

- Effective rent (after 5% vacancy): $1,710

Results:

- Monthly cash flow: -$18 (negative!)

- Cash-on-cash return: -0.4%

- Cap rate: 6.5%

- DCR: 1.08

- Break-even ratio: 96%

This property "passes" the 1% rule but loses money every month. The combination of high property taxes, higher insurance (older coastal property), and maintenance reserves eats up all the rent income. The 96% break-even ratio means you have almost no margin for error—any vacancy or unexpected expense puts you further underwater.

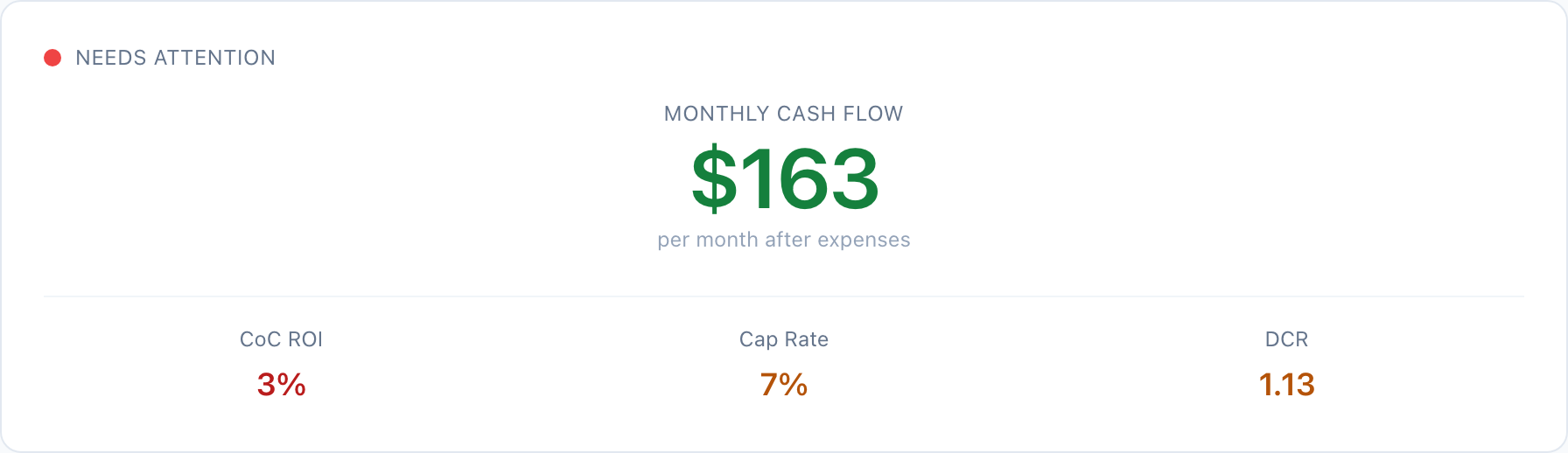

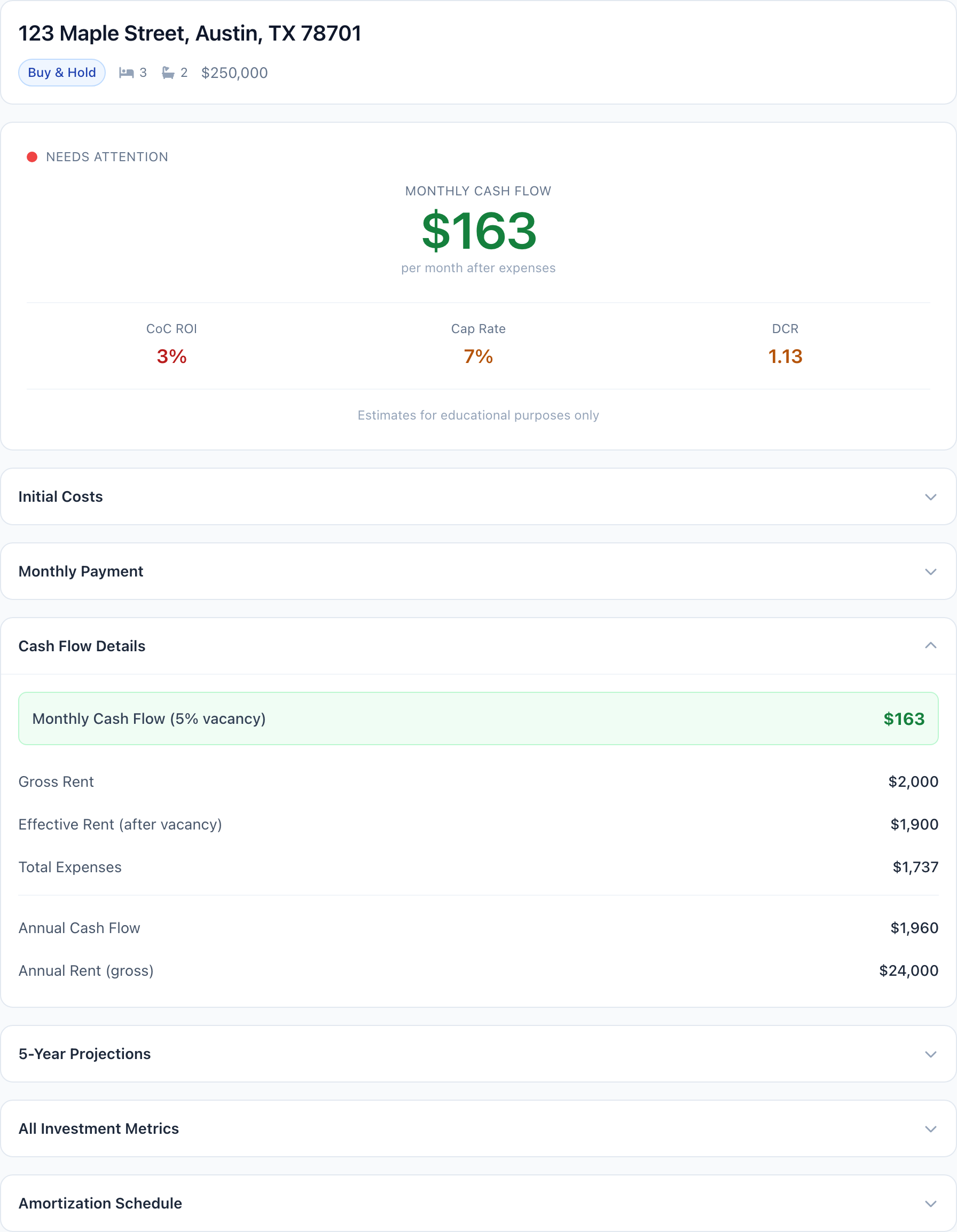

Property B: Fails the 1% rule

- Purchase price: $250,000

- Monthly rent: $2,000 (0.8%, fails 1% rule)

- Property taxes: $2,400/year (0.96% rate - landlord-friendly state)

- Insurance: $1,200/year (newer construction)

- Maintenance reserve: $100/month (newer property, less upkeep)

- 25% down at 7% interest

Monthly breakdown:

- P&I: $1,248

- Taxes: $200

- Insurance: $100

- Maintenance: $100

- Property management: $200

- Total expenses: $1,848

- Effective rent (after 5% vacancy): $1,900

Results:

- Monthly cash flow: $52

- Cash-on-cash return: 0.9%

- Cap rate: 6.2%

- DCR: 1.04

- Break-even ratio: 92%

This property "fails" the 1% rule but actually produces positive cash flow. Lower taxes and insurance in a landlord-friendly state make a significant difference. While the 92% break-even is still tight, it's better than Property A's 96%.

The lesson: The 1% rule would have told you to buy Property A (which loses money) and skip Property B (which makes money). Neither property is a home run at current rates, but Property B is clearly the better choice. The 1% rule gave you exactly the wrong answer.

A note on current market reality: You might notice that even Property B has modest returns. This is the reality of investing at 7% interest rates. The days of easy cash flow are over. But that does not mean investing is dead—it means you need better analysis to find the deals that actually work. A 0.9% cash-on-cash return plus equity building plus appreciation can still beat other investments. You just cannot rely on simple rules to find these deals.

When simple rules help (and when they hurt)

Simple rules like the 1% rule have one valid use: initial screening when you have dozens of properties to review.

If you are scanning 50 listings, you might use 0.7% or 0.8% as a quick filter. Properties below that threshold are unlikely to cash flow in any scenario, so you save time by skipping them.

But that is where the usefulness ends. Once you have a shortlist of 5-10 properties worth analyzing, you need real metrics. Cash-on-cash return. Cap rate. DCR. Break-even ratio. Actual monthly cash flow based on actual expenses.

The 1% rule cannot tell you if a deal works. It can only tell you if a deal might be worth calculating.

The real skill: analyzing more deals faster

If better metrics require more calculation, how do you keep up?

This is where most new investors struggle. They know they should analyze deals properly. But building spreadsheets takes time. So they either:

- Analyze a few deals thoroughly and miss opportunities

- Use shortcuts like the 1% rule and make mistakes

- Get overwhelmed and stop looking altogether

The solution is tools that do the math instantly. Enter a property's details once, and see cash-on-cash return, cap rate, DCR, break-even ratio, and cash flow immediately. No spreadsheet formulas. No manual calculations.

CrescoRealty calculates all these metrics automatically. You can analyze a property in under 60 seconds, see exactly where it stands, and make informed decisions without guessing.

Key takeaways

-

The 1% rule does not work in most 2026 markets. Prices rose faster than rents, breaking the math.

-

Simple rules hide complexity. Two properties with the same rent-to-price ratio can have very different returns.

-

Use multiple metrics instead: Cash-on-cash return, cap rate, DCR, and break-even ratio each tell you something important.

-

A property can "fail" the 1% rule and still be profitable. And vice versa.

-

Speed matters. The ability to analyze deals quickly means you can evaluate more properties and find the ones that actually work.

Ready to move beyond the 1% rule?

Stop filtering deals with outdated shortcuts. See the metrics that actually matter for every property you consider.

Get started free and analyze your first property in under 60 seconds.